India’s capex engine sputters, except for these two sectors

This cautious stance is mainly due to soft domestic demand and ongoing geopolitical uncertainty, said experts. This trend is also reflected in India Inc.’s restrained spending on fixed assets as a proportion of revenue.

According to a Mint analysis of 400 BSE-500 firms (excluding those in banking, financial services, and insurance), their spending on fixed assets (such as land, equipment, and plants)—a key measure of capital expenditure— has declined significantly since the pandemic. The ratio dropped from nearly 6% in FY20 to a low of 4.8% in FY24, inching up slightly to 5.2% by FY25. This ratio’s median stood at 4.8% across the post-pandemic period.

The narrowing breadth of private capital expenditure signals corporate hesitation to invest in capacity expansion amid uncertain post-pandemic demand, keeping most firms on the sidelines, noted experts.

Broader slump

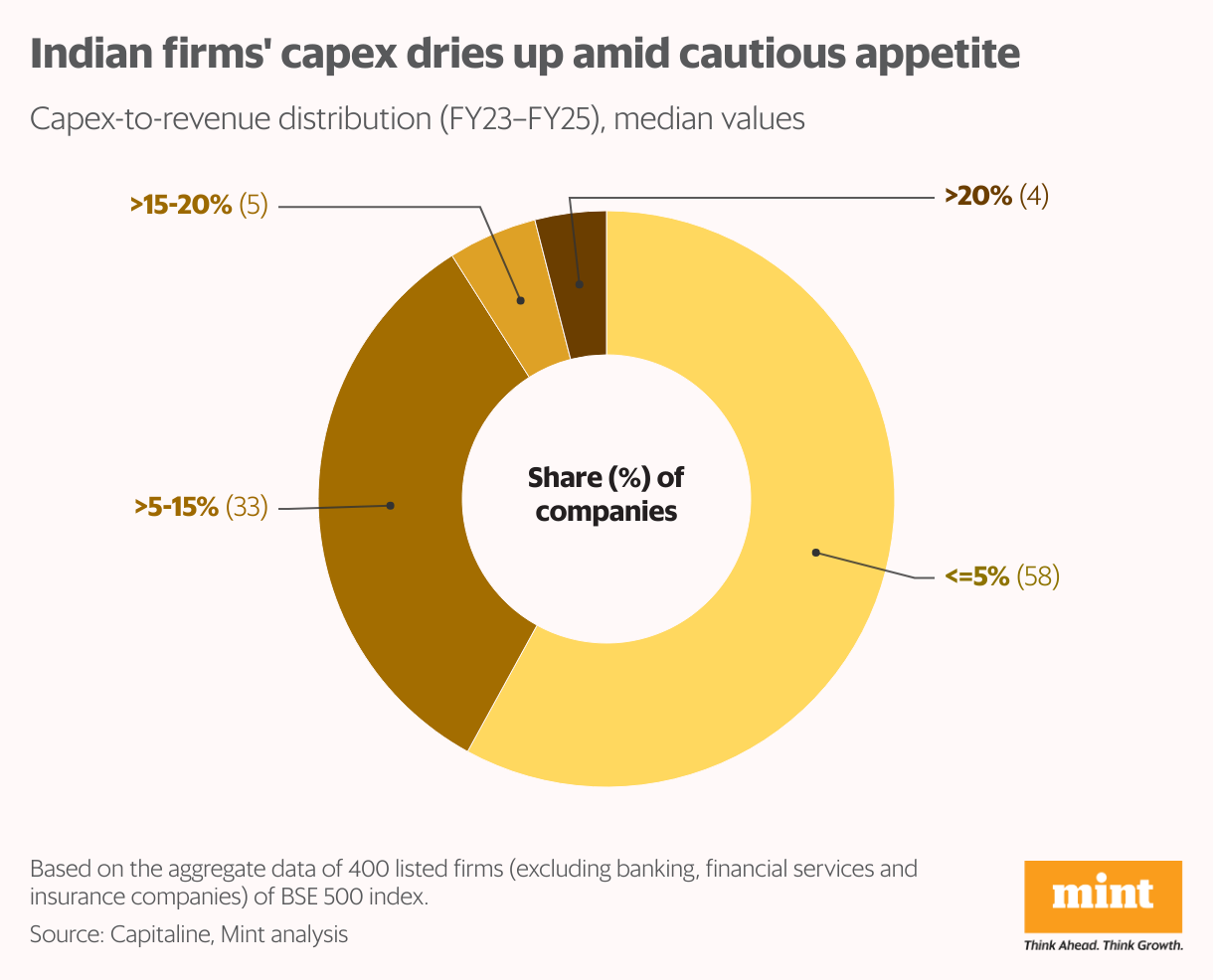

At a deeper level, the caution becomes clear: a staggering 58% of companies—nearly six out of every ten—typically committed just 5% or less of their revenue to capital expenditure between FY23 and FY25. Their decision to keep their powder dry highlights a widespread and persistent trend of corporate timidity amid uncertainties.

This pool largely comprises sectors traditionally less capital-intensive, such as IT, FMCG, consumer durables, and agriculture and allied sectors. Crucially, however, even capital-heavy sectors like automobiles, capital goods, and oil and gas have joined this cautious majority post-Covid, mirroring India’s weak consumption and uneven industrial activity.

Meanwhile, one-third of India Inc (33% of companies) occupied the crucial middle band, committing between 5% and 15% of their revenue to capex over the last three years, on a median basis.

This middle band has emerged as India Inc’s investment sweet spot, housing a blend of fast-growing and consumer-facing sectors. For instance, consumer-facing industries like retail sit just above the 5% threshold, while healthcare and travel, both riding strong demand tailwinds, spent around 6–7%.

This puts their typical capex in line with traditional heavyweights like metals and mining. Additionally, chemicals and textiles saw outlays of 7% and 10%, respectively.

As you move to the higher end of the spectrum, companies willing to open the investment spigots are a rare sight. Just 5% of firms have committed between 15% and 20% of revenue to capex in the last three years, while a mere 4% reported spending in the highest bracket (above 20%).

Sectoral outliers

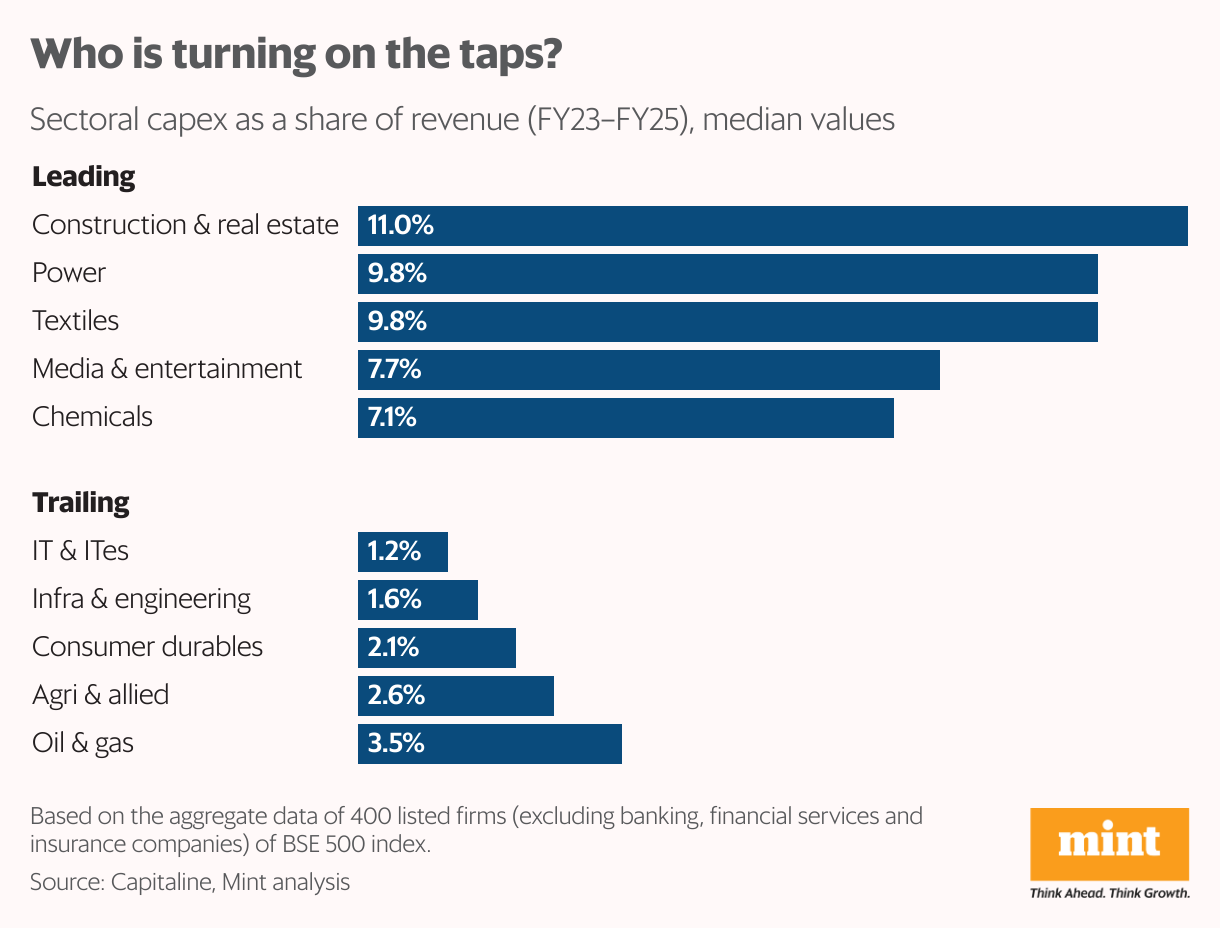

However, there are notable outliers. Among sectors, the top capex performers were real estate and power, which consistently committed around 10–11% of their revenue to capacity expansion over the last three years.

These were the only two sectors that managed to buck the broader trend of stagnation, showing consistent year-on-year increases in spending.

Ranen Banerjee, partner and economic advisory leader at PwC India sees real estate as a capex front-runner next year as well, with housing demand set to gain from falling policy rates and cheaper home loans going forward.

Power is also co-leading the charge, attracting around 40% of overall bank loan sanctions in FY25, nearly double its share of 24% in FY24, according to an IIFL Finance report.

Meanwhile, Miren Lodha, senior director at Crisil Market Intelligence, noted that infrastructure-led capex will sustain corporate spending momentum in the medium term, while production-linked incentive schemes and emerging sectors will underpin industrial capex.

The energy sector will also drive investments. “India’s rising rare earth and energy import bills are driving a decadal push into alternate energy and heavy green power investments,” said Vivek Iyer, partner and financial services risk leader at Grant Thornton Bharat. “Meanwhile, our high-end manufacturing drive is powering an upswing in chips, defence, and aerospace investments.”

Notably, telecommunication services, defence, aerospace engineering and marine port services have consistently contributed to India Inc’s capex over the last five years, Mint’s analysis showed. But while new-age sectors are gaining momentum, their scale remains modest versus legacy industries, whose investment value has shrunk sharply over the past decade, noted the IIFL report.

Going forward, experts believe the latest Goods and Services Tax (GST) and income-tax relief at lower slabs, along with softer policy rates, will soon lift disposable incomes and spur consumption. “This could provide a second-order boost to manufacturing capex in automobiles, appliances and electronics,” said Shahzad Madon, CEO of TCG Asset Management.

However, Grant Thorton Bharat’s Iyer expects business sentiment to remain muted during US President Donald Trump’s presidency, limiting private investment. “We expect private capex to be slow in 2026,” he said.

“With global volatility persisting, government spending will remain crucial in sustaining private capex within India,” he added.

Post Comment